Introduction to Blockchain Technology

- Blockchain technology represents a transformative approach to digital transactions and data management. At its core, a blockchain is a decentralized ledger that records transactions across a network of computers. This structure is key to enhancing the security and integrity of data, as it mitigates the risks associated with a centralized system.

- The term "blockchain" derives from its fundamental architecture: a series of "blocks" that are linked together to form a continuous "chain." Each block contains a set of records, including transaction details, timestamps, and a cryptographic hash of the previous block. This chaining mechanism ensures that alterations to any individual block would necessitate changes to all subsequent blocks, thereby reinforcing the overall security of the dataset. Each participant in the blockchain network possesses a copy of the entire ledger, which fosters transparency and trust among users.

- The inception of blockchain technology can be traced back to 2008 when it was proposed as the underlying foundation for Bitcoin, the first decentralized cryptocurrency. This innovation sought to eliminate the need for intermediaries in financial transactions, ultimately leading to increased efficiency and reduced costs. Since then, blockchain's versatility has evolved beyond cryptocurrency into various applications such as supply chain management, healthcare, and smart contracts.

- Key terms associated with blockchain include "nodes," which are individual devices connected to the network that validate and relay transactions, and "ledgers," which represent the entire record of all transactions maintained within the blockchain ecosystem. Understanding these concepts is crucial for grasping the broader implications and functionalities of blockchain technology in contemporary society.

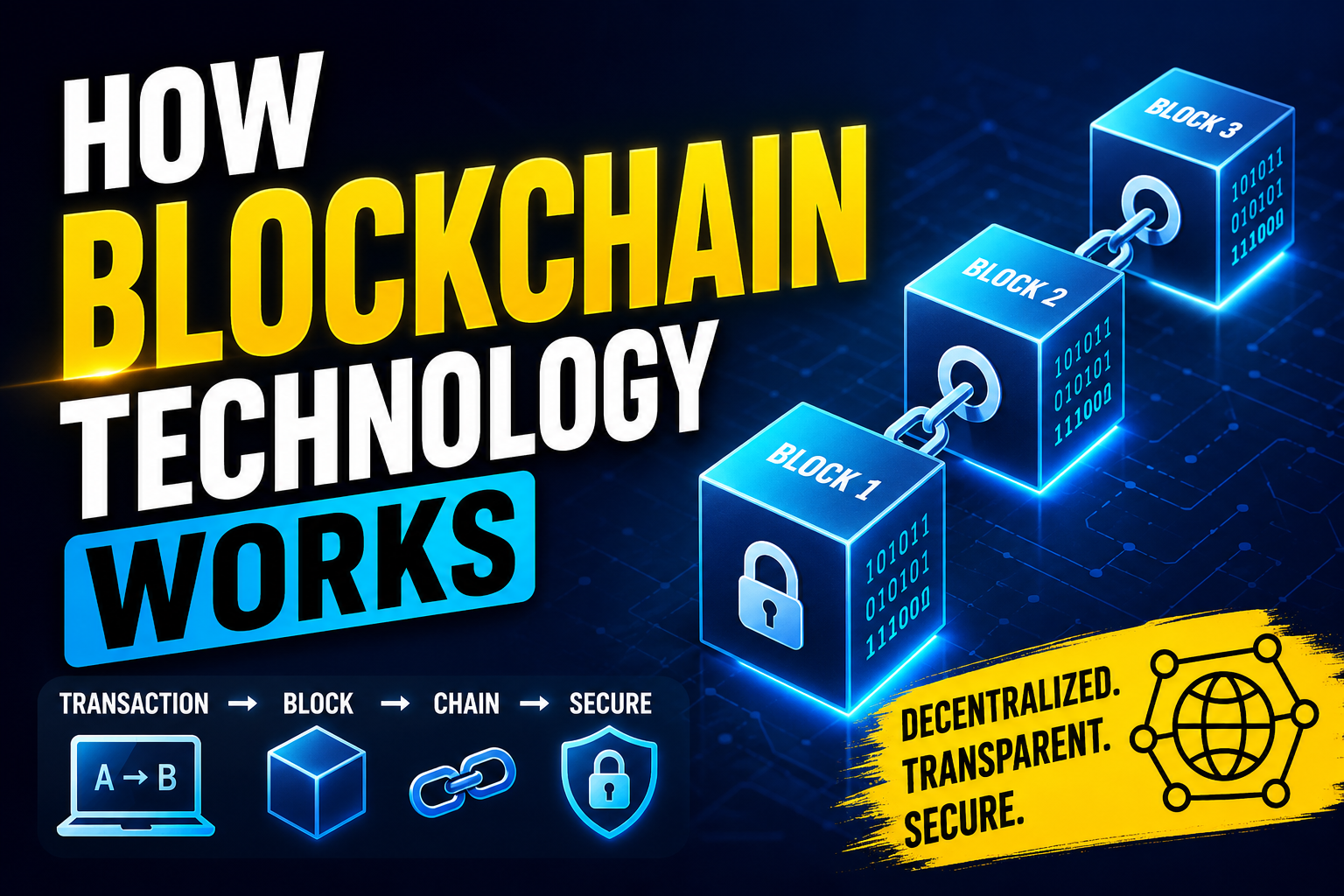

The Structure of a Blockchain

- A blockchain, at its core, is a decentralized and distributed digital ledger technology that securely records transactions across a network of computers. Understanding the structure of a blockchain requires analyzing its fundamental components which include blocks, chains, and nodes.

- Each block within a blockchain serves as a container for a collection of data. This data typically encompasses a list of transactions, a timestamp, and a unique cryptographic hash that links the block to its predecessor. The formation of a block occurs through a process called mining, where computers—often called miners—solve complex mathematical problems to validate the transactions recorded within it. Once a block is successfully mined, it is added to the chain, forming an interlinked series of transactions.

- The unique hash of each block ensures that any alteration within its contents will result in a completely different hash value. Consequently, this feature safeguards the integrity of the blockchain, as any attempt to modify a block would also necessitate changes to all subsequent blocks, making unauthorized alterations practically impossible. Additionally, the timestamp added to each block affirms the chronological order of the transactions, providing an immutable record that can be verified by anyone within the network.

- Thus, a blockchain’s structure is specifically designed to maintain the security and accuracy of the data while ensuring transparency for all participating users. The decentralized nature of blockchain technology eliminates the need for a central authority, allowing users to engage directly with the system while maintaining trust through cryptographic verification. By securely linking blocks and employing a consensus mechanism, blockchain fosters a reliable method for recording information, paving the way for various applications beyond cryptocurrency, including supply chain management, healthcare, and finance.

How Transactions Work in Blockchain

- Blockchain technology relies on a decentralized structure to manage transactions efficiently and securely. When a user initiates a transaction, the details, such as sender, recipient, and amount, are recorded as a block of data. This block is then broadcast to a network of computers known as nodes. Each node maintains a copy of the blockchain, enabling consensus and verification among them.

- After the transaction is initiated, it enters a pool of unconfirmed transactions known as the mempool. Miners, or nodes that validate transactions, select transactions from this pool based on specific criteria, often prioritizing those with higher transaction fees. The chosen transactions are bundled together into a new block, ready for verification.

- The verification process involves complex algorithms designed to ensure that the proposed blocks are valid. Each node in the network checks the proposed block's contents against its existing copy of the blockchain. Specifically, nodes verify the transaction history of the sending address to guarantee that the sender has sufficient funds and that the transaction adheres to the blockchain's consensus protocol. This mechanism is critical in preventing double spending—a scenario where the same coin is spent more than once—ensuring the integrity of the transaction.

- Once a block has successfully passed the verification process, it is added to the blockchain, and all nodes update their copies to reflect this addition. This immutable ledger ensures transparency and security, as altering any information in a previously confirmed block would require a consensus from the majority of the network's nodes, making such fraudulent activity practically impossible. Thus, the collaborative effort among nodes, combined with robust verification mechanisms, guarantees secure and reliable transaction processing in blockchain technology.

Consensus Mechanisms Explained

- Consensus mechanisms are fundamental to blockchain technology as they provide the means for decentralized networks to reach agreement on the validity of transactions and the state of the blockchain. This section discusses the most widely used consensus mechanisms: Proof of Work (PoW) and Proof of Stake (PoS), along with additional alternatives.

- Proof of Work is the original consensus mechanism, which underpins cryptocurrencies like Bitcoin. PoW requires miners to solve complex mathematical problems to validate transactions and create new blocks. While PoW is highly secure due to its gradual difficulty, it consumes a substantial amount of energy and time. Critics argue that this energy-intensive process makes it unsustainable and limits scalability, prompting the exploration of alternatives.

- In contrast, Proof of Stake offers a more eco-friendly approach. In PoS, validators are chosen to confirm transactions based on the number of coins they hold and are willing to "stake" as collateral. This method significantly reduces energy consumption and allows faster transaction speeds. However, PoS can lead to centralization, as those with greater stakes may have increased influence, potentially undermining the democratic nature of blockchain.

- Other notable consensus mechanisms include Delegated Proof of Stake (DPoS), where stakeholders elect delegates to validate transactions, and Practical Byzantine Fault Tolerance (PBFT), which is designed for permissioned networks and aims to ensure consensus even when some participants may act maliciously. Each consensus method has distinct benefits and drawbacks, and the choice of mechanism largely depends on the network’s specific goals regarding decentralization, security, and efficiency.

The Role of Cryptography in Blockchain Security

- Cryptography plays a pivotal role in the security and integrity of blockchain technology. It is the backbone that enables secure transactions, protects sensitive information, and fosters trust among participants in the network. The effectiveness of a blockchain system largely relies on cryptographic principles, which include hash functions, digital signatures, and public/private key pairs.

- Hash functions are essential cryptographic tools that convert input data into a fixed-length string of characters, commonly referred to as a hash. Each block in a blockchain contains a hash of the previous block, creating a chain that secures the integrity of the entire dataset. Any alteration in the data would result in a drastically different hash, signaling tampering attempts and enhancing the resilience of the blockchain against attacks.

- Another critical aspect of blockchain security is the use of digital signatures. These signatures allow participants to verify the authenticity and integrity of transactions. When a user initiates a transaction, their private key is used to create a unique digital signature associated with that transaction. This signature can be verified by others using the corresponding public key, ensuring that only the rightful owner can authorize the transaction. This process not only safeguards the identity of the user but also helps in preventing fraud.

- Public/private key pairs are foundational elements in cryptographic operations within blockchain networks. The public key is shared openly, enabling others to send cryptocurrency or data securely, while the private key is kept secret, granting the user control over their assets. This duality of keys provides an additional layer of security, making unauthorized access and manipulation significantly more challenging.

- In conclusion, cryptography is integral to maintaining the security and integrity of blockchain systems. By employing hash functions, digital signatures, and public/private key pairs, blockchain technology ensures robust protection against fraud and cyber threats, thereby instilling confidence in its users.

Types of Blockchain Networks

- Blockchain technology has evolved significantly, giving rise to various types of blockchain networks, each tailored to specific use cases and functionalities. Broadly, these networks can be classified into three primary categories: public blockchains, private blockchains, and consortium blockchains.

- Public blockchains, as the name suggests, are open for anyone to participate. They are decentralized and operate independently of any central authority. This characteristic ensures that data entered into the blockchain is immutable and transparent. Notable examples include Bitcoin and Ethereum, which facilitate decentralized finance and serve as platforms for a variety of decentralized applications. Public blockchains are ideal for applications where transparency, security, and inclusiveness are paramount.

- On the other hand, private blockchains are restricted to a specific group of participants. Access is typically controlled, meaning that only authorized entities can engage with the network. This type of blockchain is frequently used within organizations or between a limited consortium of businesses. For example, many enterprises utilize private blockchains for supply chain management and internal record-keeping, as these applications benefit from the speed and efficiency of a controlled environment while still harnessing the advantages of blockchain technology.

- Lastly, consortium blockchains represent a hybrid between public and private networks. They are governed by a group of organizations that collectively manage access and permissions. Consortium blockchains are often employed in industries where collaboration and shared data integrity are vital, such as banking or healthcare. By allowing multiple stakeholders to participate while maintaining a level of control, consortium blockchains help streamline processes, reduce redundancy, and foster trust among participants.

- This categorization of blockchain networks sheds light on the diverse applications and functional strengths of blockchain technology. By understanding these types, stakeholders can determine the most appropriate blockchain solution for their specific needs and objectives.

Real-World Applications of Blockchain Technology

- Blockchain technology has rapidly evolved beyond its initial use in cryptocurrency, showcasing its versatility through a variety of applications across numerous industries. One prominent example is in the financial sector, where blockchain provides a secure and transparent way to conduct transactions. By eliminating intermediaries, financial institutions can lower costs, increase transaction speeds, and reduce fraud, all while maintaining the integrity of sensitive data.

- In supply chain management, blockchain facilitates enhanced traceability and accountability. Companies can utilize blockchain to track goods as they move through the supply chain, ensuring that every stage of production and delivery is recorded. This transparency helps in verifying the authenticity of products, combatting counterfeit goods, and enhancing trust between stakeholders. For instance, major retailers have implemented blockchain to track the journey of their products from sourcing to consumer, enabling them to quickly identify issues, such as recalls.

- Healthcare is another sector where blockchain technology is beginning to make significant strides. By providing a secure platform for storing patient records, healthcare providers can ensure that sensitive data is only accessible to authorized personnel. This not only protects patient privacy but also allows for seamless sharing of information across healthcare systems, improving the overall quality of care. Additionally, blockchain can be used to track pharmaceuticals, ensuring that medications are authentic and safe for patients.

- Moreover, various industries such as real estate, energy, and even entertainment are exploring blockchain's potential to streamline operations and improve security. For instance, in real estate, smart contracts facilitated by blockchain simplify property transactions, reducing the need for lengthy paperwork while decreasing the likelihood of disputes. In the energy sector, decentralized energy trading models can be implemented, empowering consumers to sell excess energy directly to other users.

- These examples illustrate that blockchain technology has extensive real-world applications across diverse sectors, highlighting its potential to transform traditional business practices. As research continues and more organizations recognize the benefits of blockchain, its impact is expected to grow further, transforming industries for the better.

Challenges and Limitations of Blockchain Technology

- While blockchain technology offers significant benefits, it is not without its challenges and limitations. One of the primary concerns is scalability. As more transactions are added to the blockchain, the network must process an increasing amount of data. This can lead to slower transaction speeds and increased costs, especially for large-scale applications. For example, Bitcoin and Ethereum have faced scalability issues during peak times, resulting in transaction backlogs and higher fees for users.

- Energy consumption is another pressing issue associated with blockchain networks, particularly those utilizing proof-of-work consensus mechanisms. The computational power required to validate transactions and secure the network consumes vast amounts of energy. This has raised concerns regarding the environmental impact of blockchain technology, propelling discussions around sustainable alternatives, such as proof-of-stake, which consumes significantly less energy.

- Additionally, regulatory hurdles represent a significant obstacle for the adoption of blockchain technology. Governments worldwide are still grappling with how to classify cryptocurrencies and blockchain applications, which can create uncertainty for businesses looking to invest in this technology. Without a clear regulatory framework, stakeholders may be hesitant to fully engage with blockchain solutions, thereby stalling innovation and broader acceptance.

- Interoperability is another critical challenge. Multiple blockchain systems often operate in silos, lacking the ability to effectively communicate with one another. This fragmentation can inhibit the seamless exchange of information and value across different networks, limiting the full potential of blockchain applications. For the technology to achieve widespread adoption, efforts must be made to create standards and protocols that allow disparate blockchain systems to work together.

The Future of Blockchain Technology

- The future of blockchain technology promises to be transformative, with various innovations and applications advancing its adoption across different sectors. One of the most significant developments is the rise of smart contracts. These self-executing contracts with predefined terms embedded in code facilitate secure and automatic transactions without intermediaries. As industries explore their potential, the efficiency and trustworthiness of smart contracts can revolutionize sectors such as real estate, insurance, and supply chain management.

- Another emerging trend is the rapid growth of decentralized finance (DeFi). This paradigm shift enables traditional financial services, such as lending and trading, to occur on blockchain platforms without a central authority. By leveraging smart contracts and innovative protocols, DeFi platforms aim to enhance accessibility to financial services globally, offering users greater control over their assets. The expansion of DeFi also has the potential to democratize financial systems, making them more inclusive for unbanked individuals and communities.

- Moreover, the increasing integration of blockchain technology in global economies cannot be overlooked. Governments and enterprises are beginning to recognize the advantages of blockchain in enhancing transparency and reducing fraud. By implementing blockchain solutions, industries can streamline operations, increase efficiency, and ensure data integrity. As more organizations adopt blockchain technology for activities like supply chain tracking, identity verification, and smart governance, we can expect a significant shift in how various sectors operate.

- In conclusion, the future of blockchain technology appears promising, with advancements in smart contracts, decentralized finance, and broader economic integration leading the way. As these trends continue to evolve, their impact will be felt across multiple industries, suggesting that blockchain is poised to redefine traditional practices for years to come.

Login or create account to leave comments

Comments (0)